Who Regulates Pre-Settlement Funding? Top Insights

Who regulates pre settlement funding? The truth is, pre-settlement funding is mostly unregulated in the United States. Unlike traditional loans, there’s no federal standard governing the industry. Instead, state-level regulations are the primary form of oversight, with only a handful of states setting clear guidelines. For instance, Ohio and Nebraska have specific disclosure and licensing requirements, while states like Wisconsin enforce transparency through legal acts.

Pre-settlement funding provides financial help to lawsuit plaintiffs waiting for their case to settle. As it gains popularity, understanding who watches over this industry becomes crucial for consumers.

Who regulates pre settlement funding terms at a glance:

– how does pre settlement funding work

– is pre settlement funding a loan

– pre settlement lenders

Understanding Pre-Settlement Funding

Pre-settlement funding is a unique financial tool designed to help plaintiffs manage their expenses while waiting for their lawsuits to resolve. It’s particularly beneficial in personal injury claims, where the financial strain can be significant due to medical bills, lost wages, and other costs.

Non-Recourse Advances

One of the key features of pre-settlement funding is that it is a non-recourse advance. This means that if you don’t win or settle your case, you don’t have to repay the advance. Unlike traditional loans, there’s no requirement for monthly payments, and your credit history doesn’t affect your eligibility. Instead, the strength of your legal case is what matters most.

Financial Relief

For many plaintiffs, this funding provides crucial financial relief. It allows them to cover essential living expenses, such as:

- Rent or mortgage payments

- Utility bills

- Medical expenses

- Everyday living costs

Without this financial support, plaintiffs might feel pressured to settle their cases too early, often for less than they deserve. Pre-settlement funding can give them the breathing room they need to negotiate a fair settlement.

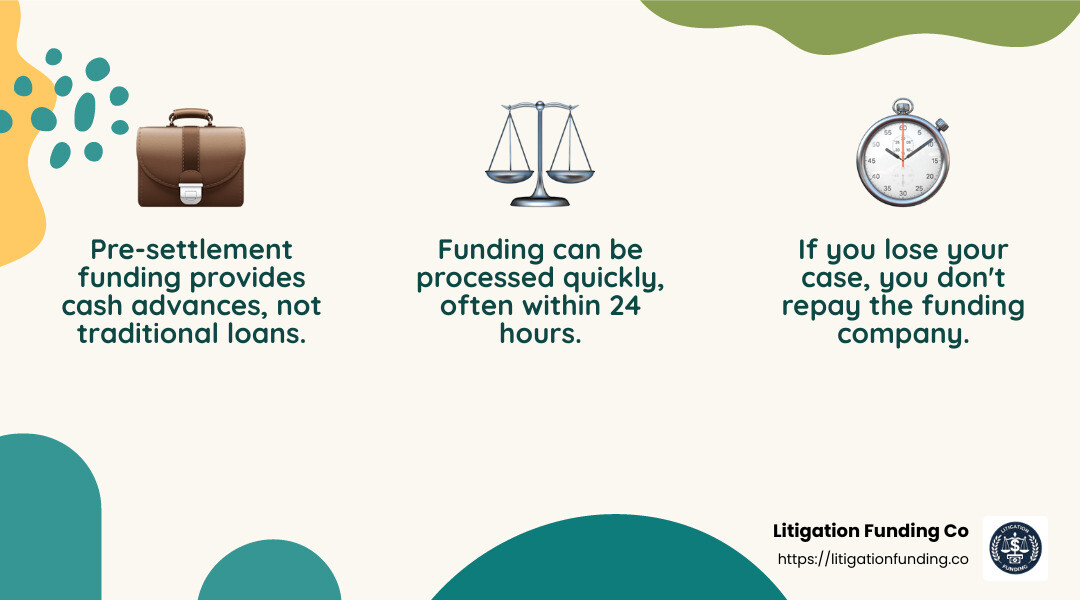

Pre-settlement funding is not a traditional loan. Instead, it’s an advance on the potential settlement or court award. This distinction is important because it shifts the risk from the plaintiff to the funding company. If the case is unsuccessful, the plaintiff owes nothing.

In summary, pre-settlement funding offers a lifeline to those caught in lengthy legal battles, providing much-needed financial stability and allowing plaintiffs to focus on their recovery and the pursuit of justice.

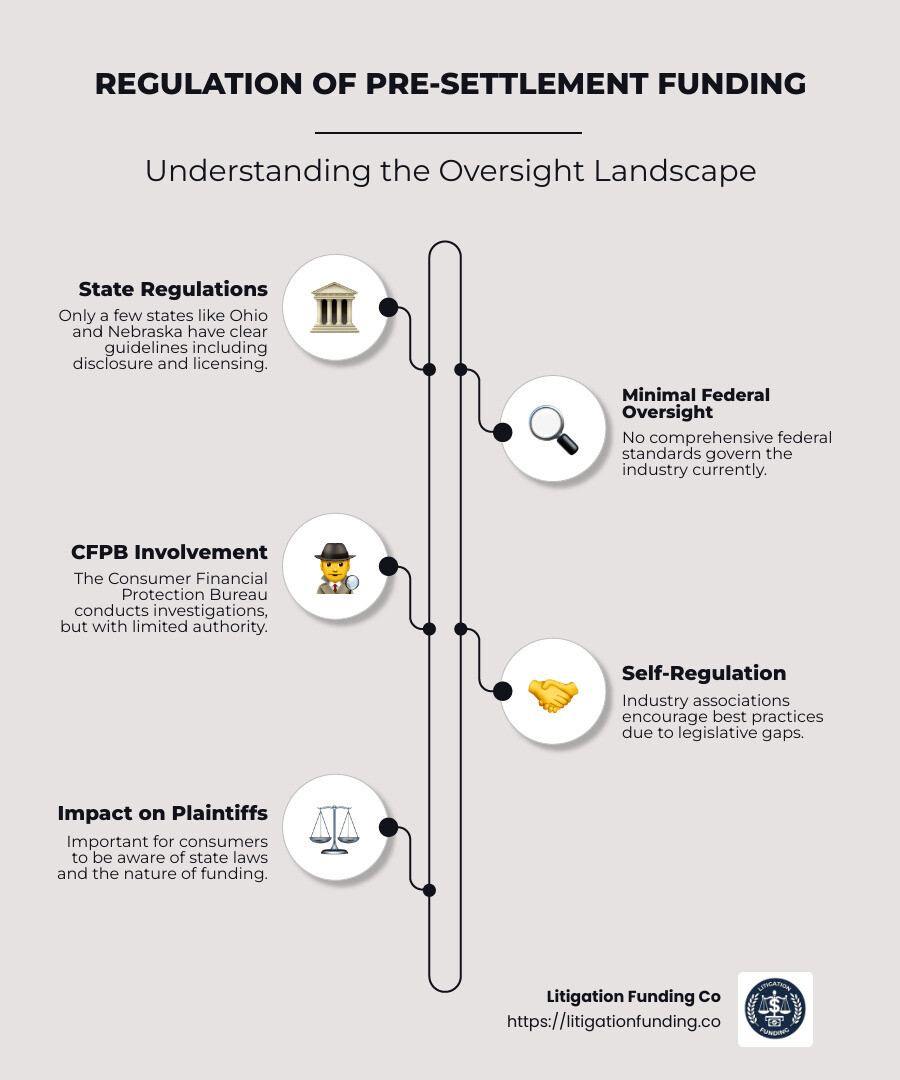

Who Regulates Pre-Settlement Funding?

When it comes to who regulates pre-settlement funding, the landscape is a bit of a patchwork. Unlike traditional loans, pre-settlement funding isn’t uniformly regulated across the United States. Instead, it falls under a mix of state-level regulations, some federal oversight, and a degree of self-regulation within the industry.

State Regulations

A handful of states have taken steps to regulate pre-settlement funding. These regulations vary widely, reflecting different levels of consumer protection and industry oversight.

- Maine, Nebraska, Ohio, Oklahoma, Tennessee, and Wisconsin are among the states with specific laws governing pre-settlement funding. In these states, regulations often focus on transparency and fairness. For instance, lenders might be required to disclose terms clearly and offer a cooling-off period during which borrowers can cancel the agreement without penalty.

- In Nebraska and Ohio, pre-settlement loan companies must provide disclosures, be licensed, and allow borrowers five business days to cancel the agreement. Oklahoma goes a step further by prohibiting loan companies from paying referral fees to law firms or participating directly in litigation.

- Tennessee and Wisconsin have regulations, but critics argue that they may not offer sufficient consumer protection.

These state-level regulations aim to protect consumers from potentially exploitative practices, ensuring that plaintiffs fully understand the terms of their funding agreements.

Federal Oversight

At the federal level, oversight is still emerging. The Consumer Financial Protection Bureau (CFPB) has started to show interest in the industry, signaling that it may step in to address potential abuses.

- The CFPB has taken legal action against some funding companies, arguing that the cash advances they offer could fall under its jurisdiction. This is part of a broader effort to investigate and potentially regulate the industry more closely.

- Notable cases, like those against RD Legal and Access Funding, highlight the CFPB’s growing involvement. These cases often revolve around whether pre-settlement advances should be considered loans or financial products subject to federal oversight.

Self-Regulation

Given the lack of comprehensive federal regulation, self-regulation is an essential part of the industry. Many reputable pre-settlement funding companies voluntarily adhere to best practices, focusing on transparency, ethical behavior, and fair terms for plaintiffs.

While self-regulation can help maintain industry standards, it’s not a substitute for formal oversight. Plaintiffs seeking pre-settlement funding should always conduct thorough research and consult with their attorneys to ensure they’re working with a reputable company.

In the next section, we’ll dive into how pre-settlement funding works, exploring the processes and criteria involved in securing a cash advance during a lawsuit.

How Pre-Settlement Funding Works

Pre-settlement funding can be a lifeline for plaintiffs waiting on a lawsuit settlement. This type of funding is unique because it provides cash advances rather than traditional loans. Here’s a look at how it all comes together.

Non-Recourse Nature

One of the most significant features of pre-settlement funding is its non-recourse nature. This means that if you lose your case, you owe nothing back to the funding company. Unlike a standard loan, where you’d be responsible for repayment regardless of the outcome, pre-settlement funding uses your expected settlement as collateral. This setup shifts the risk to the funding company.

Application Process

The process to secure pre-settlement funding is generally straightforward, but it involves a few key steps:

- Attorney Involvement: Your attorney plays a crucial role. They provide the necessary information about your case to the funding company. This includes details like the nature of your claim, the expected settlement amount, and the timeline for resolution.

- Funding Company Evaluation: The funding company will evaluate the risk associated with your case. They assess the likelihood of a favorable settlement and the potential amount you might receive. This evaluation helps determine how much money they can advance to you.

- Cash Advance: Once your application is approved, you receive a cash advance. This can often be processed quickly, sometimes within 24 hours.

- No Repayment if Case Lost: If your case doesn’t end in a settlement or favorable verdict, you don’t have to repay the advance. This feature makes pre-settlement funding a low-risk option for those in need of financial relief during lengthy legal proceedings.

Pre-settlement funding offers a way to manage financial stress without the burden of traditional loans. However, because it’s not heavily regulated, work with reputable companies and consult with your attorney to ensure you understand the terms.

In the next section, we’ll weigh the pros and cons of pre-settlement funding, helping you decide if it’s the right choice for your situation.

Pros and Cons of Pre-Settlement Funding

Pre-settlement funding can be a real lifesaver when you’re waiting for your lawsuit to settle. But like anything, it has its ups and downs. Let’s break it down.

Benefits

Financial Relief

One of the biggest perks is the immediate financial relief it offers. If you’re struggling to pay bills or cover living expenses like rent, groceries, or medical costs, this funding can help. It allows you to focus on your recovery and your legal case without the stress of money worries.

No Repayment if You Lose

Thanks to its non-recourse nature, you don’t have to repay the advance if you lose your case. This means less risk for you, especially if you’re already in a tough financial spot.

Negotiation Leverage

Having extra funds can give your attorney more time to negotiate a better settlement. Without financial pressure to settle quickly, you might end up with a more favorable outcome.

Drawbacks

High Interest Rates

On the flip side, pre-settlement funding can come with high interest rates. Some plaintiffs face rates as steep as 60% per year. This can eat into your final settlement amount, leaving you with less than you expected.

Minimal Regulation

The lack of strict regulation in this area means that rates and terms can vary widely. Some states have consumer protection laws, but not all. This can make it tricky to steer and potentially risky.

Reduced Settlement Recovery

The combination of high interest rates and additional fees can significantly reduce the amount you ultimately receive from your settlement. You might find that after repaying the funding company, there’s not much left for you.

Pre-settlement funding is a mixed bag. It offers crucial financial relief but can also come with costly downsides. Carefully consider these factors and consult with your attorney to decide if it’s the right path for you.

In the next section, we’ll tackle some frequently asked questions about pre-settlement funding, addressing common concerns and clarifying how it all works.

Frequently Asked Questions about Pre-Settlement Funding

Can my lawyer deny me from getting a pre-settlement loan?

Your lawyer cannot outright deny you from seeking a pre-settlement loan. However, their involvement is crucial. Lawsuit funding companies need to communicate with your attorney to evaluate the strength of your case. This means your lawyer must provide case details and evidence to help the funding company make an informed decision.

While your lawyer can’t stop you, they can offer valuable advice. It’s wise to discuss your decision with them to understand the potential impact on your case and settlement.

What happens if I lose my case?

One of the key benefits of pre-settlement funding is its non-recourse nature. Simply put, if you lose your case, you don’t have to repay the loan. The risk falls on the funding company, not you. This provides peace of mind, knowing you won’t be financially burdened if the lawsuit doesn’t go in your favor.

Are pre-settlement loans regulated by the government?

Pre-settlement loans are subject to minimal regulation, which means the rules can differ significantly from state to state. Some states have specific laws to protect consumers, but many do not. This lack of uniform regulation can lead to variations in interest rates and terms, making it essential to thoroughly understand any agreement before signing.

Consult your attorney and do your research to ensure you’re working with a reputable funding company that offers fair terms. Check if your state has specific laws regarding pre-settlement funding to better understand your rights and protections.

Now that we’ve covered these common questions, let’s explore how pre-settlement funding works and what you need to know about the process.

Conclusion

At SeaCoast Financial, we understand that waiting for a lawsuit to settle can be financially stressful. That’s why we offer quick funding solutions to help you cover essential expenses during this challenging time. Our process is designed to be straightforward and efficient, ensuring you receive the financial support you need without unnecessary delays.

Transparency is at the heart of what we do. We believe in clear communication and fair terms, with no hidden fees or surprises. Our team works closely with your attorney to ensure you fully understand the funding agreement before you sign it. This collaboration helps protect your interests and ensures you make informed decisions.

Choosing the right pre-settlement funding company is crucial. With us, you benefit from our commitment to a transparent process and our focus on delivering the financial relief you need.

If you’re facing financial challenges while waiting for your lawsuit to conclude, don’t hesitate to explore our pre-settlement funding options. We’re here to provide the support you need to focus on what truly matters—your recovery and your case.

{kind=link}

{kind=link}

{kind=link}