sba loan no credit check: Top 5 Opportunities in 2024

SBA Loans with No Credit Check: Myths and Realities

When it comes to sba loan no credit check, many business owners have questions. Here’s a quick answer: Most SBA loans do require a credit check, but there are rare exceptions. For small businesses struggling with poor credit, navigating these waters can be challenging. However, understanding the landscape can open up opportunities for securing funding.

Here’s what you need to know right off the bat:

- Credit Checks Are Typically Required: SBA loans usually involve a hybrid credit check that includes both your business and personal credit scores.

- Strict Eligibility Criteria: Even when credit checks are avoided, other stringent requirements like time in business, revenue streams, and a solid business plan are non-negotiable.

- Alternatives Exist: If SBA loans aren’t an option due to credit issues, there are other types of funding to consider, such as merchant cash advances and crowdfunding.

Why is this important?

Securing funding is a cornerstone for any business, especially those looking to grow or recover. Poor credit history can often be a roadblock, but knowing your options empowers you to move forward. Understanding how to steer SBA loans and other financing options can make the difference between struggling and thriving.

Challenges

- High Competition: Small business grants, which don’t require credit checks or repayment, attract stiff competition.

- Strict Standards: Even when credit checks are not considered, other criteria can be challenging.

- Potential High Costs: Alternative funding options may come with higher interest rates or stringent repayment terms.

Opportunities

- Diverse Options: Beyond SBA loans, entrepreneurs can explore grants, microloans, and alternative financing.

- Support Systems: Access to resources like SBA Export Finance Managers can offer custom guidance.

I’m Haiko de Poel, an expert in simplifying complex funding topics. With experience in marketing strategy and business development, I specialize in creating informative, accessible content that breaks down barriers to understanding business finance.

Now, let’s dig deeper into what makes SBA loans unique and explore your financing options.

Simple sba loan no credit check glossary:

– business loan without credit check

– no credit check funding

– start up business loans with no credit check

Understanding SBA Loans

SBA loans are a popular choice for small businesses seeking funding due to their competitive terms and supportive resources. Here’s a breakdown of the types, eligibility, benefits, and application process for these loans.

Types of SBA Loans

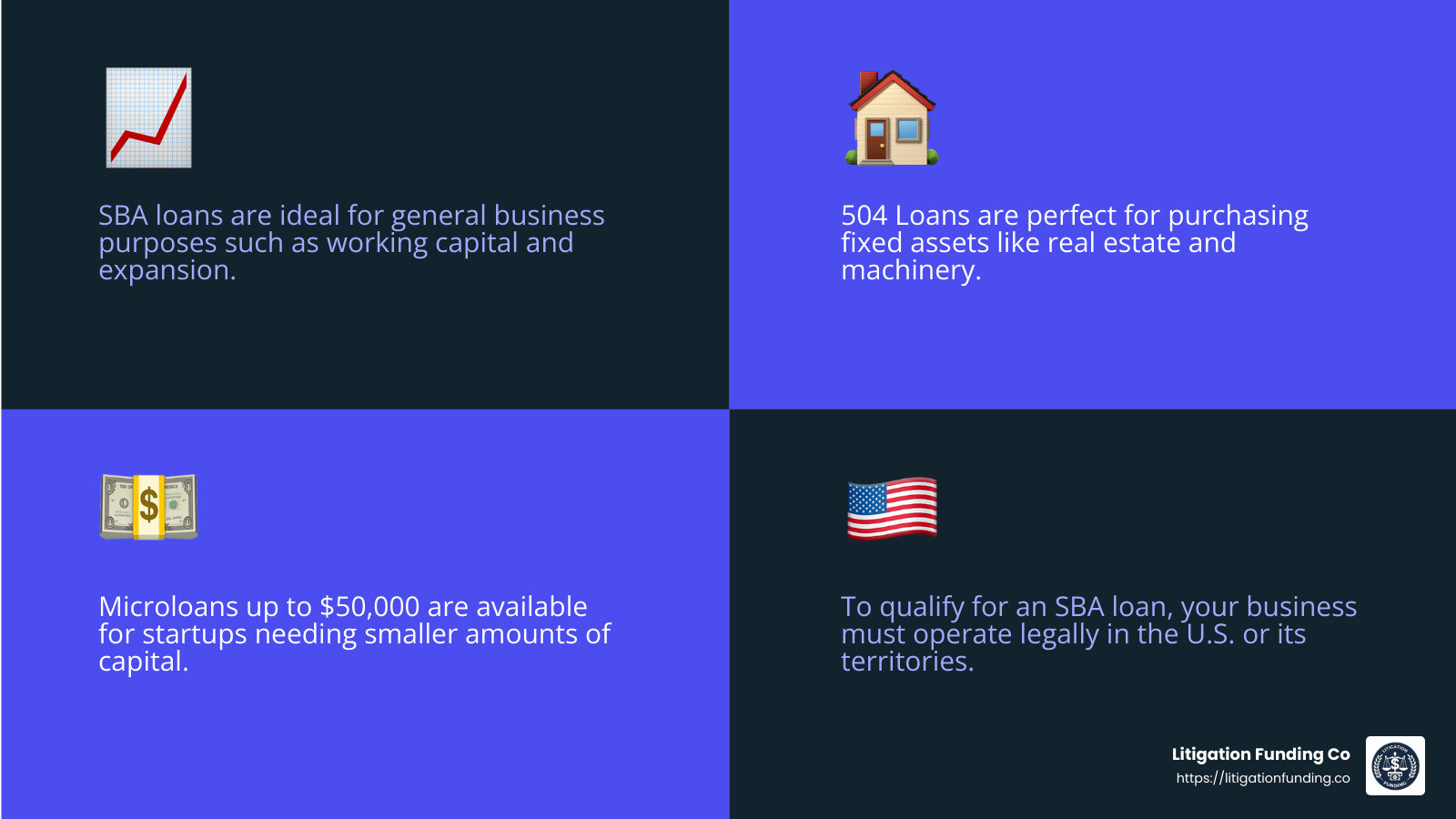

1. 7(a) Loans:

The most common type, ideal for general business purposes such as working capital, expansion, and equipment purchases.

2. 504 Loans:

Designed for purchasing fixed assets like real estate and machinery. These loans offer long-term, fixed-rate financing through Certified Development Companies (CDCs).

3. Microloans:

Small loans up to $50,000, perfect for startups and small businesses needing smaller amounts of capital. These are provided by intermediary lenders.

Eligibility

To qualify for an SBA loan, businesses generally need to meet the following criteria:

- For-Profit Business: The business must be officially registered and operate legally.

- U.S. Operations: The business must be physically located and operate in the United States or its territories.

- Creditworthiness: The business must have a sound credit history, though specific requirements can vary by loan type.

- Exhaust Financing Options: The requested loan should be unavailable on reasonable terms from non-government sources.

Benefits of SBA Loans

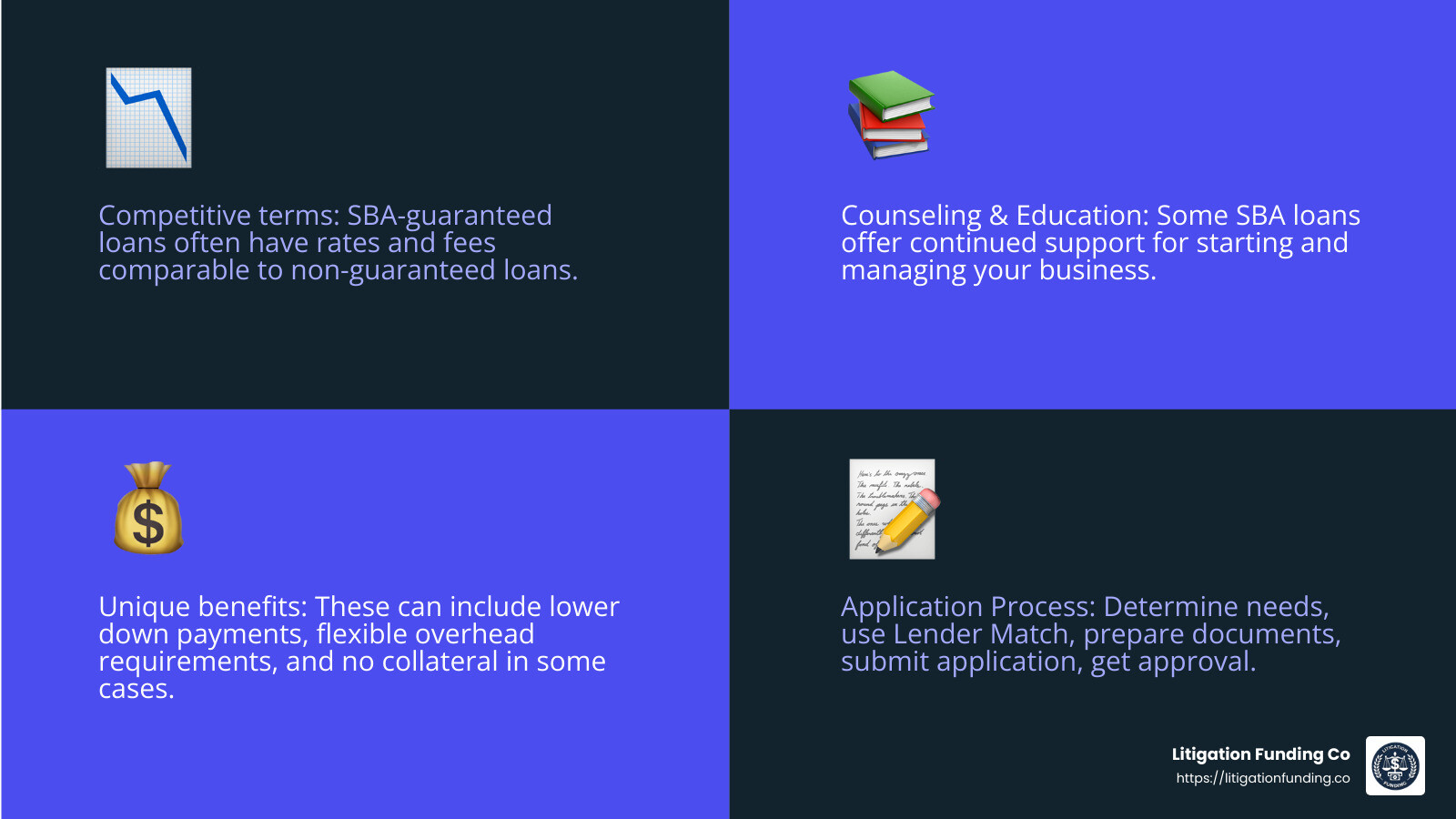

1. Competitive Terms:

SBA-guaranteed loans often come with rates and fees that are comparable to non-guaranteed loans.

2. Counseling and Education:

Some loans include continued support to help you start and run your business effectively.

3. Unique Benefits:

These can include lower down payments, flexible overhead requirements, and in some cases, no collateral needed.

Application Process

1. Determine Your Needs:

Identify why you need the loan and how much funding you require.

2. Use Lender Match:

Enter basic information about your business on the SBA’s Lender Match tool to connect with potential lenders.

3. Prepare Documentation:

Gather necessary documents such as business plans, financial statements, and tax returns.

4. Submit Application:

Create an account and start talking to interested lenders to submit your application.

5. Approval and Management:

Once approved, work with your lender to manage and repay the loan.

Understanding these aspects of SBA loans can help you steer the process more effectively and increase your chances of securing the funding you need.

SBA Loan No Credit Check: Is It Possible?

When it comes to securing an SBA loan with no credit check, things can get tricky. Understanding the role of credit checks in SBA loans and exploring available alternatives can help you steer this complex landscape.

Credit Checks

Most lenders perform a credit check when you apply for a business loan. For SBA loans, this usually includes both personal and business credit checks. Credit checks help lenders assess the risk of lending to you. If your credit risk is high, lenders might deny your application or charge higher interest rates.

Fact: Some SBA lenders may require a minimum FICO score of 680 and a FICO Small Business Scoring Service (SBSS) score of 160 to qualify for certain loans.

SBA Requirements

The SBA itself doesn’t issue loans but guarantees them, making it easier for small businesses to get approved. However, lenders have their own criteria, which often include credit checks. Here’s a quick look at what they generally expect:

- Personal and Business Credit Scores: Most SBA loans require a credit check to evaluate your financial history.

- Collateral: Depending on the loan type and amount, collateral might be necessary.

- Personal Guarantee: This means you’re personally responsible for repaying the loan if your business can’t.

Alternatives to SBA Loans with No Credit Check

If your credit score isn’t up to par, you might consider other financing options that don’t require a credit check. Here are some alternatives:

1. Merchant Cash Advances (MCAs):

These are based on future sales and don’t usually require a credit check. However, they can be expensive due to high fees and short repayment terms.

2. Invoice Factoring:

This involves selling your unpaid invoices to a lender. It’s a good option if you have outstanding invoices but need cash quickly.

3. Equipment Financing:

If you need to purchase equipment, some lenders offer financing based on the value of the equipment rather than your credit score.

4. Crowdfunding:

Platforms like Kickstarter allow you to raise money from individuals without a credit check. This can be a viable option if you have a compelling business idea.

5. Business Grants:

Grants are funds you don’t have to repay and don’t require a credit check. However, they are highly competitive and often require a detailed application.

Misconceptions

There are some common misconceptions about SBA loans and credit checks:

1. “Guaranteed Approval”:

Be wary of lenders who promise guaranteed approval without a credit check. These offers are often predatory, with high-interest rates and hidden fees.

2. “No Credit Check Means No Risk”:

Loans without credit checks can still be risky. They often come with higher costs and stricter repayment terms.

3. “SBA Loans Can Be Used for Anything”:

SBA loans have specific uses, like working capital, equipment purchases, and real estate. Personal expenses are not allowed.

Fact: Even for SBA loans, some microlenders might be more flexible with credit requirements, but they still perform some form of credit evaluation.

Understanding these nuances can help you make informed decisions and explore viable alternatives if your credit score is a hurdle.

Next, we’ll dive into how you can qualify for SBA loans even with bad credit.

Types of No Credit Check Business Loans

If your credit score isn’t stellar, don’t worry. There are several no credit check business loans available that can help you secure the funding you need. Here are some of the most common types:

Merchant Cash Advances (MCAs)

Merchant cash advances provide a lump sum of cash in exchange for a percentage of your future sales. Lenders assess your daily or monthly sales to determine the advance amount.

Pros:

– No credit check required.

– Quick access to cash.

– Flexible repayment based on sales.

Cons:

– High fees and interest rates.

– Short repayment terms.

Example: PayPal Working Capital offers advances based on your PayPal sales history. You could receive funds within minutes with flexible repayment options.

Invoice Factoring

Invoice factoring involves selling your unpaid invoices to a factoring company. In return, you get immediate cash, typically around 70-90% of the invoice value. The factoring company then collects the payment directly from your clients.

Pros:

– Quick access to funds.

– No credit check required.

– Approval based on your clients’ creditworthiness.

Cons:

– Fees ranging from 2.5% to 5%.

– Factoring company interacts with your clients, which might affect relationships.

Example: A small manufacturing business sells $10,000 worth of invoices to a factoring company and receives $8,500 upfront. The factoring company collects payment from the clients, taking a fee for their service.

Equipment Financing

Equipment financing is designed for businesses looking to purchase equipment, such as heavy machinery or computers. Some lenders are more flexible when it comes to credit scores and may not require a credit check.

Pros:

– No credit check required.

– Equipment itself serves as collateral.

– Can help build business credit.

Cons:

– Limited to equipment purchases.

– Higher interest rates if credit is poor.

Example: A construction company needs a new excavator. They get equipment financing, using the excavator as collateral, without undergoing a credit check.

Business Grants

Business grants are funds you don’t have to repay, often provided by government agencies, nonprofits, or private companies. They don’t require a credit check but are highly competitive.

Pros:

– No repayment required.

– No credit check needed.

– Can provide significant funding.

Cons:

– Highly competitive.

– Extensive application process.

Example: A small business owned by a veteran receives a $10,000 grant from a nonprofit organization supporting veteran entrepreneurs.

These no credit check business loans can be excellent alternatives if your credit score is less than ideal. Next, we’ll explore how you can qualify for SBA loans even with bad credit.

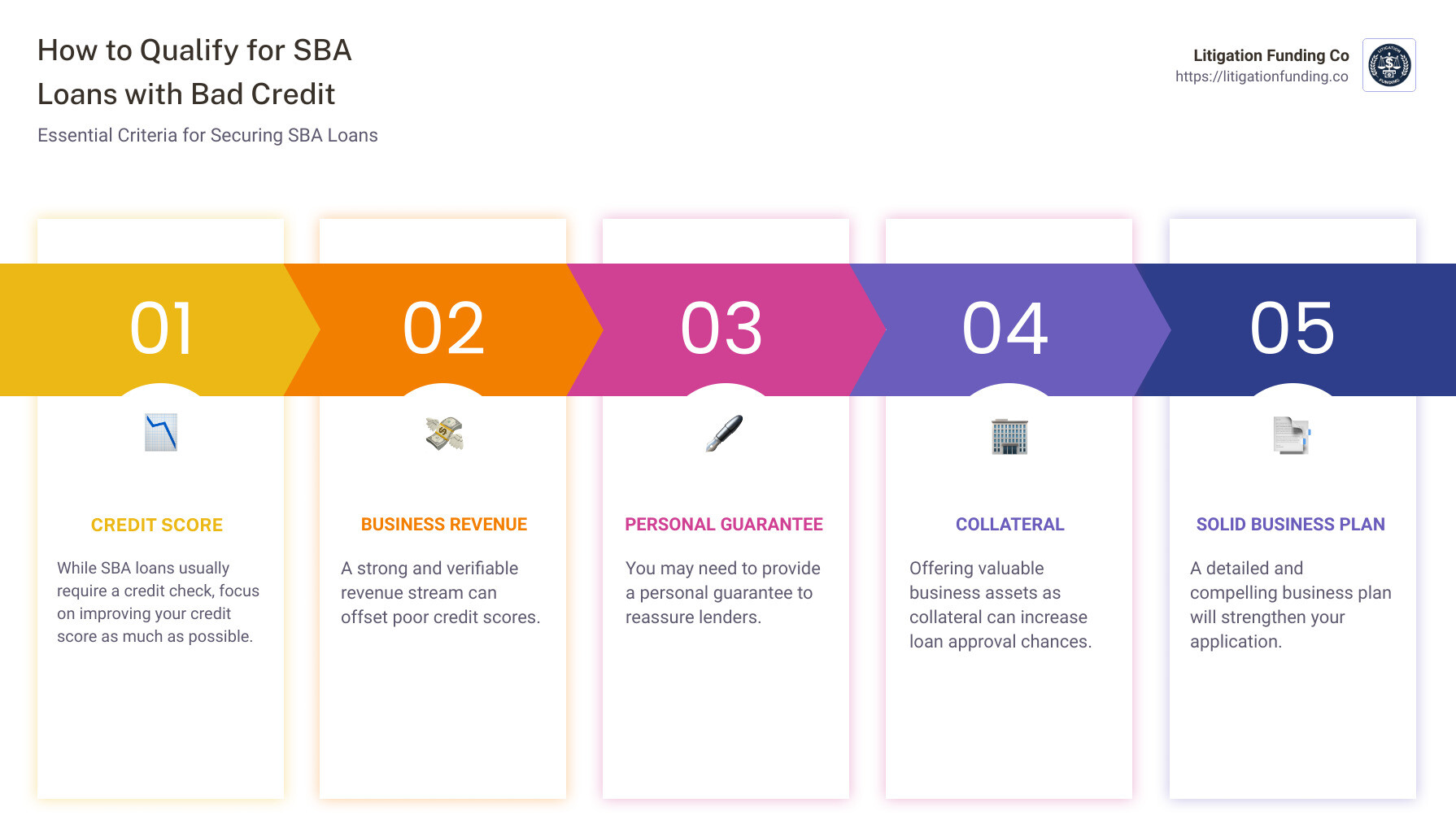

Securing an SBA loan with bad credit can be challenging, but it’s not impossible. Here’s what you need to know to improve your chances:

Credit Score

Credit scores are a critical factor for most lenders. While the SBA itself doesn’t set a minimum credit score, many lenders require a FICO score of at least 620. But don’t be discouraged if your score is lower. Some lenders might focus on other aspects of your financial profile.

Tip: Improve your credit score by paying off debts, disputing inaccuracies on your credit report, and keeping your credit utilization low.

Business Revenue

Lenders often look at your business revenue to assess your ability to repay the loan. Consistent and strong revenue streams can sometimes offset a low credit score.

Fact: Some lenders may require you to show monthly business revenue of at least $15,000 to qualify for an SBA loan.

Tip: Keep detailed financial records and be prepared to show your business’s growth and profitability.

Personal Guarantee

A personal guarantee means you are personally responsible for repaying the loan if your business can’t. This can help lenders feel more secure and may improve your chances of approval.

Tip: Be sure you understand the risks involved with a personal guarantee before agreeing to it.

Collateral

Offering collateral can also increase your chances of getting an SBA loan. Collateral can be business assets like equipment, inventory, or real estate.

Fact: According to the SBA, collateral is required for all loans over $25,000.

Tip: Make an inventory of your business assets to determine what you can offer as collateral.

Additional Tips

- Prepare a Solid Business Plan: A well-crafted business plan can show lenders your strategy for success and how you plan to use the loan funds.

- Seek Counseling and Education: Some SBA loans come with ongoing support to help you manage your business effectively. Use these resources to strengthen your application.

By focusing on these areas, you can improve your chances of qualifying for an SBA loan even with bad credit. Next, we’ll explore alternative financing options for businesses with poor credit.

Alternative Financing Options for Businesses with Poor Credit

If you have poor credit, getting traditional financing can be tough. But don’t worry—there are still options. Here are some alternative financing solutions that don’t rely heavily on your credit score.

Business Lines of Credit

Business lines of credit are flexible and can be a lifeline for businesses with poor credit. They work like a credit card: you get a set limit and can draw from it as needed. You only pay interest on the amount you use.

Pros:

– Flexible use of funds

– Pay interest only on the drawn amount

– Can help manage cash flow

Cons:

– May require a minimum revenue

– Higher interest rates for poor credit

Example: Some lenders offer lines of credit for businesses with a minimum credit score of 600. You can borrow between $1,000 and $500,000.

Microloans

Microloans are small loans, typically up to $50,000, aimed at helping small businesses and startups. They often come with lower interest rates and more flexible terms.

Pros:

– Lower interest rates

– Flexible terms

– Support for underserved communities

Cons:

– May require a personal guarantee or collateral

– Application process can be more detailed

Example: The U.S. Small Business Administration (SBA) offers microloans through nonprofit organizations.

Retirement Account Loans

If you have a retirement account, like a 401(k), you might be able to borrow against it to fund your business. Retirement account loans have some unique features:

Pros:

– No credit check required

– Lower interest rates compared to other loans

– Repayment terms that can extend up to five years

Cons:

– Risk of penalties and taxes if you can’t repay

– Impact on future savings

Example: Borrowing from your 401(k) can provide quick access to funds without affecting your credit score.

Vendor Financing

Vendor financing involves your suppliers offering short-term credit for the products you purchase from them. Terms like Net-30 give you 30 days to pay.

Pros:

– No personal credit check

– Builds business credit

– Improves cash flow

Cons:

– Limited to purchasing from specific vendors

– Short repayment terms

Example: Many vendors offer Net-30 terms, giving you a month to pay for goods or services.

Exploring these alternative financing options can help you find the best way to fund your business, even with poor credit. Next, we’ll answer some frequently asked questions about SBA loans for businesses with no credit check.

Frequently Asked Questions about SBA Loans for Businesses with No Credit Check

Do SBA loans require a credit check?

Yes, SBA loans do require a credit check. The SBA guarantees loans issued by banks and other financial institutions, and these lenders will review your credit history to assess your creditworthiness. Both your personal and business credit scores may be evaluated.

However, some lenders might be more flexible. For example, SBA microlenders often have less stringent credit requirements. But generally, a credit check is part of the process.

Can I get an SBA loan with bad credit?

Getting an SBA loan with bad credit is challenging but not impossible. The SBA itself doesn’t set a minimum credit score, but individual lenders do. Some lenders may require a minimum FICO score of 680, while others might be more lenient.

Example: SBA microlenders may be more willing to work with businesses that have lower credit scores, as they focus on supporting underserved communities.

To improve your chances:

– Improve your business revenue: Strong financials can offset a lower credit score.

– Offer collateral: Providing assets as collateral can make lenders more comfortable.

– Personal guarantee: Be ready to personally guarantee the loan, which means you’ll be responsible for repayment if your business can’t pay.

What are the easiest SBA loans to get approved for?

The easiest SBA loans to get approved for are typically those with more flexible requirements, such as SBA microloans and Community Advantage loans.

SBA Microloans: These are designed for small businesses and startups needing smaller loan amounts, usually up to $50,000. They often have more flexible credit requirements and are provided through nonprofit organizations.

Community Advantage Loans: These loans aim to support businesses in underserved markets. They have higher approval rates for businesses with lower credit scores and offer loans up to $250,000.

Example: The SBA Community Advantage program is designed to help small businesses in underserved areas, making it easier for those with less-than-perfect credit to get approved.

By understanding these options and preparing your application accordingly, you can improve your chances of securing an SBA loan, even with poor credit.

Conclusion

Navigating business loans can be daunting, especially when credit checks are involved. While SBA loans are a fantastic resource for small businesses, they typically require a credit check, which can be a hurdle for some. However, the SBA offers various programs like microloans and Community Advantage loans that are more lenient towards businesses with lower credit scores.

SeaCoast Financial understands the unique challenges faced by small business owners. Just like our pre-settlement funding options, which provide financial relief without credit checks, there are alternative business financing options available that also don’t rely on credit scores.

Final Thoughts

If you find yourself struggling to secure an SBA loan due to credit issues, remember there are other avenues to explore. At SeaCoast Financial, our mission is to ease your financial burden, allowing you to focus on what truly matters—growing your business and achieving your goals. For more information and to start your application process, contact SeaCoast Financial today.

We’re committed to helping you steer your financial journey with confidence and ease.

{kind=link}

{kind=link}

{kind=link}

{kind=link}