Borrow Money Until Settlement: Top 5 Essential Facts 2024

Financial Relief When You Borrow Money Until Settlement

Borrow money until settlement can provide much-needed financial relief during a pending lawsuit. Whether you’re dealing with medical bills, living expenses, or other urgent costs, this option can offer a lifeline.

Here’s a quick breakdown of what you need to know if you’re considering a settlement loan:

- Get a cash advance on your lawsuit.

- Use the funds for any expenses you choose.

- Non-recourse loans: If you lose the case, you owe nothing.

- Quick approval and payout within 24-48 hours.

If you’re in a personal injury lawsuit and struggling with mounting bills, borrowing money until settlement can help you stay afloat financially. This type of loan allows you to cover immediate costs without stressing about repaying the loan if your case doesn’t win.

In this guide, we’ll explore what settlement loans are, how they work, the benefits and drawbacks, and other alternatives. By the end, you’ll have a clear understanding of whether this financial tool is right for you.

I’m Haiko de Poel, a seasoned marketing professional with a proven track record. Over the years, I’ve helped many understand complex financial products like borrowing money until settlement. Let’s break down everything you need to know to make an informed decision.

Borrow money until settlement word guide:

– advance lawsuit funding

– plaintiff advance funding

– easy lawsuit funding

What is a Settlement Loan?

A settlement loan is a type of cash advance provided to plaintiffs involved in ongoing lawsuits. These loans, also known as lawsuit loans, pre-settlement funding, or litigation financing, are designed to help you cover essential expenses while you await the resolution of your case.

How It Works

Unlike traditional loans, settlement loans are non-recourse. This means that if you lose your case, you don’t have to repay the loan. Instead, the repayment comes from the settlement amount or court award if you win.

Key Terms

- Cash Advance: The amount of money you receive upfront based on the estimated value of your case.

- Lawsuit Loan: Another term for a settlement loan, emphasizing its role as a financial lifeline during litigation.

- Pre-Settlement Funding: Funding provided before the settlement of a lawsuit, allowing plaintiffs to cover immediate expenses.

- Litigation Financing: A broader term that includes various financial products designed to support plaintiffs during legal proceedings.

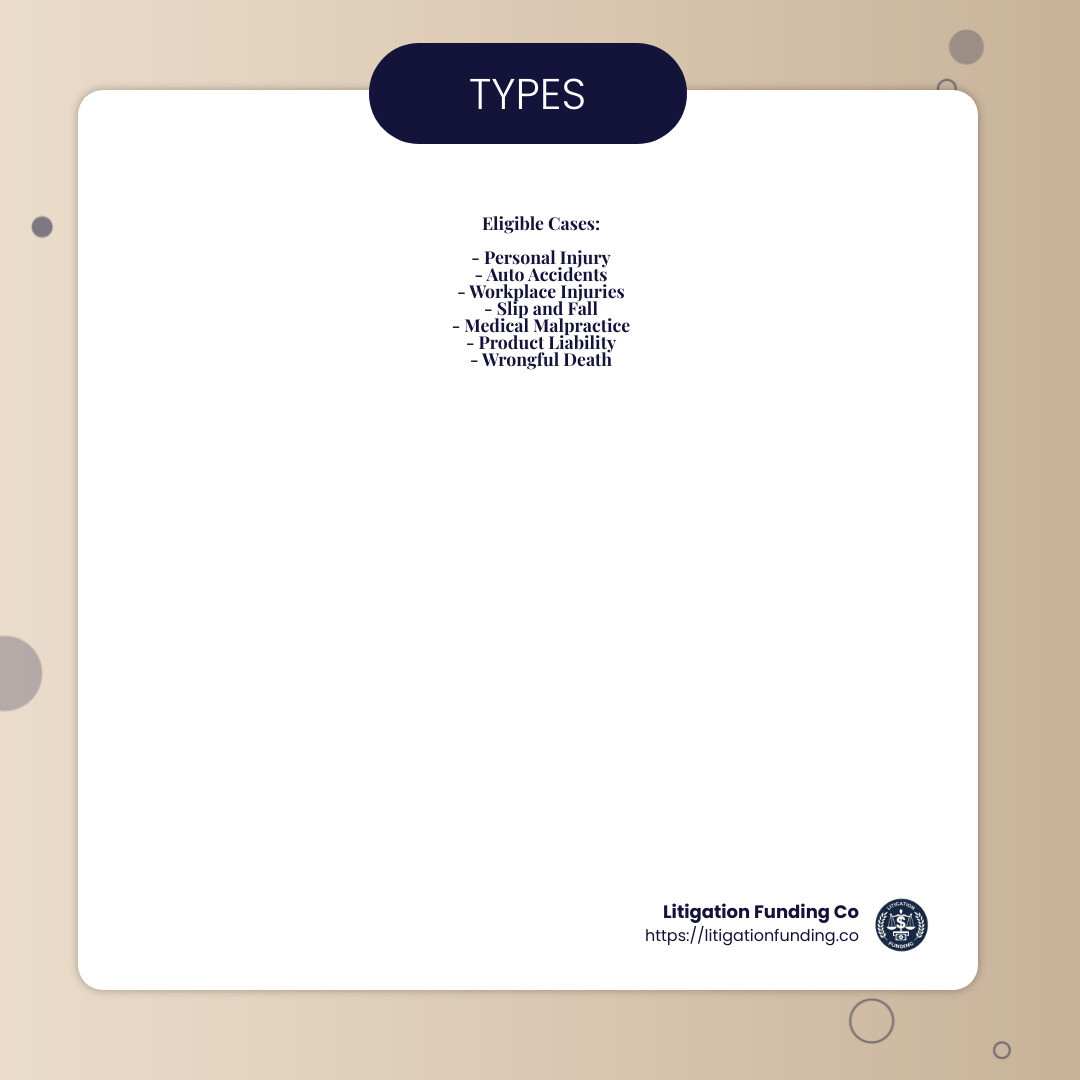

Types of Cases Eligible

Settlement loans can be used for a variety of cases, including:

- Personal Injury: Injuries due to someone else’s actions.

- Auto Accidents: Injuries from car crashes.

- Workplace Injuries: Injuries sustained at work.

- Slip and Fall: Injuries from accidents on someone else’s property.

- Medical Malpractice: Injuries due to healthcare providers’ negligence.

- Product Liability: Injuries from defective products.

- Wrongful Death: Loss of a loved one due to someone else’s actions or negligence.

Benefits and Drawbacks

Settlement loans offer several benefits, such as providing immediate financial relief and not requiring a credit check. However, they also come with high-interest rates and fees, which can eat into your final settlement amount.

In the next section, we’ll dive into how these loans work, including the application process, case evaluation, interest rates, and repayment terms. Stay tuned to understand the full picture and make an informed decision.

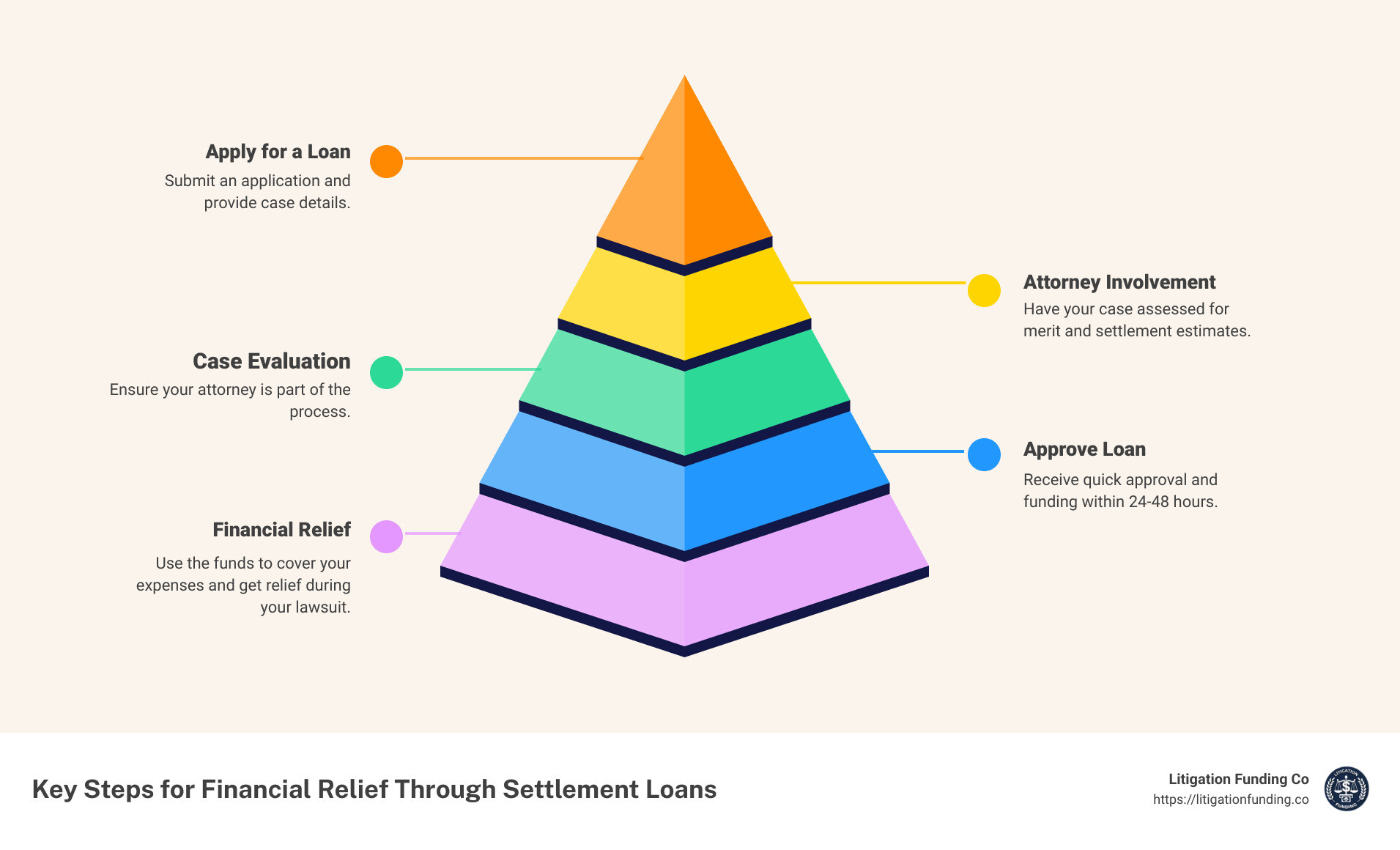

How Do Settlement Loans Work?

Application Process

Applying for a settlement loan is straightforward and quick. Here’s how it works:

-

Start Your Application: You can begin the process online or by calling the funding company. You’ll need to provide basic information about your case and your contact details.

-

Notify Your Lawyer: Inform your attorney that you’ve applied for pre-settlement funding. This ensures they are prepared when the funding company reaches out for more details.

-

Attorney Involvement: Your attorney will need to provide case specifics, including the expected settlement amount and other relevant details. This cooperation helps the funding company evaluate your case accurately.

-

Submit Case Details: Provide any available documents, such as court filings, medical records, and police reports. This can speed up the application review process.

Case Evaluation

Once your application is submitted, the funding company will evaluate your case. Here’s what they look at:

-

Merit Assessment: The company assesses the strength and merit of your lawsuit. They consider factors like the evidence you have and the likelihood of winning the case.

-

Settlement Estimate: Based on the information from you and your attorney, the company estimates the potential settlement amount.

-

Approval Criteria: The funding company weighs the risks involved. If they believe your case is strong and likely to settle favorably, they will approve the loan.

Interest and Fees

Settlement loans come with interest rates and fees that can add up quickly. Here’s what you need to know:

-

Interest Rates: These can range from 20% to 60% per year. The rate depends on factors like the strength of your case and how long it might take to settle.

-

Fees: There might be additional costs such as transaction fees, origination fees, and underwriting expenses. Make sure to read the fine print.

-

Repayment Structure: Interest is usually compounded monthly, which can significantly increase the total amount owed. Be aware of how these costs will impact your final settlement amount.

Repayment Terms

Repayment of a settlement loan is straightforward but comes with important conditions:

-

Settlement Proceeds: The loan, along with interest and fees, is repaid from the settlement proceeds once your case is resolved.

-

Attorney Fees and Litigation Expenses: Before the loan is repaid, other costs like attorney fees and litigation expenses are deducted from the settlement amount.

-

Non-Recourse: If you lose your case, you don’t owe anything. This makes settlement loans less risky for plaintiffs but more expensive due to the higher interest rates.

Understanding these aspects can help you steer the process and make an informed decision about borrowing money until settlement. In the next section, we’ll explore the types of cases eligible for settlement loans.

Types of Cases Eligible for Settlement Loans

Settlement loans can provide critical financial support for various types of legal cases. Here are the most common types of cases that qualify:

Personal Injury

Personal injury cases arise when someone’s actions cause you harm. This can include anything from a dog bite to a sports injury. If you’re dealing with medical bills or lost income due to a personal injury, a settlement loan can help cover your expenses while you wait for your case to settle.

Auto Accidents

Car accidents are one of the most common reasons people seek settlement loans. If you’ve been in a car crash, you might be facing high medical bills, car repair costs, and lost wages. A settlement loan can provide the funds you need to manage these expenses until your case is resolved.

Workplace Injuries

Injuries sustained at work can be financially devastating, especially if you’re unable to return to your job. Settlement loans can help you cover medical expenses, rehabilitation costs, and daily living expenses while your workers’ compensation claim is being processed.

Slip and Fall

Slip and fall accidents, or premises liability cases, occur when you get injured on someone else’s property due to their negligence. These cases can take a long time to resolve. A settlement loan can help you manage your financial needs while you wait for a fair settlement.

Medical Malpractice

Medical malpractice cases involve injuries caused by healthcare providers’ negligence, such as misdiagnosis or surgical errors. These cases are often complex and can take years to settle. A settlement loan can provide the financial support you need to cover ongoing medical treatments and other expenses.

Product Liability

If you’ve been injured by a defective product, you may have a product liability case. These cases can be challenging and time-consuming. A settlement loan can help you cover your costs while you pursue compensation from the manufacturer.

Wrongful Death

Wrongful death cases are filed when someone’s actions or negligence result in the death of a loved one. These cases can be emotionally and financially draining. A settlement loan can provide the financial relief you need to cover funeral costs, lost income, and other expenses during this difficult time.

Each of these case types can qualify for a settlement loan, providing you with the financial support you need while you wait for your case to settle. Next, we’ll explore the benefits of borrowing money until settlement.

Benefits of Borrowing Money Until Settlement

Borrowing money until settlement can be a financial lifeline when you’re waiting for your case to resolve. Here are the key benefits:

Financial Relief

When you’re involved in a lawsuit, especially one that involves personal injury, medical bills can pile up quickly. Settlement loans provide financial relief by covering:

- Living costs: Rent, groceries, utilities, and other daily expenses.

- Medical bills: Both immediate and ongoing medical expenses.

- Other essential expenses: Car repairs, childcare, and more.

This financial support allows you to focus on recovery rather than worrying about mounting bills.

No Credit Check

One of the biggest advantages of settlement loans is that they don’t require a credit check. Your credit score is irrelevant because these loans are non-recourse, meaning:

- Credit history doesn’t matter: Approval is based on the strength of your case, not your financial background.

- No repayment if you lose: If you don’t win your case, you owe nothing. This removes a significant financial risk.

This makes settlement loans accessible to people who might not qualify for traditional loans.

Quick Approval

Settlement loans are designed to provide fast funding. While traditional loans can take weeks to process, settlement loans often provide funds within 24-48 hours. This quick approval process involves:

- Simple application: Apply online or over the phone with minimal paperwork.

- Attorney involvement: Your lawyer provides case details to speed up the process.

- Immediate access to funds: Once approved, the money is quickly transferred to your account.

This rapid turnaround is crucial when you’re facing urgent financial needs.

Negotiation Leverage

Having access to funds can give you negotiation leverage in your lawsuit. When you’re not desperate for cash, you can:

- Avoid lowball offers: Defendants often make initial low offers hoping you’ll settle quickly due to financial pressure.

- Hold out for a better settlement: With financial stability, you can take the time needed to negotiate a fair settlement.

This can result in a higher payout, ultimately benefiting you in the long run.

Borrowing money until settlement can provide the financial stability you need during a challenging time. Next, we’ll look at some of the drawbacks to consider before taking out a settlement loan.

Drawbacks of Settlement Loans

While borrowing money until settlement can provide essential financial relief, it’s important to be aware of the drawbacks. Here are the key concerns you should consider:

High Interest Rates

Settlement loans often come with very high interest rates. These rates typically range from 20% to 60% per year. According to a study by University of Texas School of Law researchers, the average interest rate for settlement loans is 44%.

- Cost of Borrowing: High interest rates mean that the cost of borrowing can quickly add up. For example, if you borrow $10,000 at a 44% interest rate, you could end up paying $4,400 in interest annually.

- Accumulating Interest: The longer your case takes to settle, the more interest accrues. This can significantly reduce the amount you ultimately receive from your settlement.

Long Lawsuit Durations

Lawsuits, especially personal injury cases, can take years to resolve. During this time, interest on your settlement loan continues to accumulate.

- Years to Settle: It’s not uncommon for lawsuits to take several years before reaching a settlement or judgment. During this period, the interest on your loan keeps growing.

- Mounting Costs: As interest accumulates, the amount you owe can become substantial. If your case takes two years to settle, you might end up owing more in interest than the principal amount you borrowed.

Limited Regulation

Settlement loans are not heavily regulated, which can lead to predatory lending practices. Regulation varies by state, and some states have minimal consumer protection laws for these types of loans.

- State-Level Regulation: Only a handful of states have enacted laws to protect consumers from high interest rates and fees associated with settlement loans. For example, Arkansas, Tennessee, and West Virginia have capped interest rates on pre-settlement advances.

- Consumer Protection: Without strong regulations, borrowers are at risk of agreeing to unfavorable terms. If you encounter issues with your settlement loan, you may have limited recourse.

Understanding these drawbacks is crucial before deciding to take out a settlement loan. While they offer immediate financial relief, the long-term costs and risks can be significant.

Next, we’ll explore some alternatives to settlement loans that might be more cost-effective and less risky.

Alternatives to Settlement Loans

If you’re considering borrowing money until settlement but are wary of the drawbacks, there are several alternatives that might be more cost-effective and less risky. Here are a few options to explore:

Personal Loans

Personal loans can be a smart alternative if you have good credit. They typically offer lower interest rates compared to settlement loans, which can save you a lot of money in the long run.

- Traditional Loans: Personal loans from banks or credit unions usually come with fixed interest rates and repayment terms. This means you’ll know exactly how much you need to repay each month.

- Lower Interest Rates: Interest rates for personal loans are generally much lower than the 20-60% you might face with settlement loans. This makes them a more affordable option.

Low-Interest Credit Cards

Another option is to apply for a low-interest credit card. Some cards even offer an introductory 0% APR period.

- Intro 0% APR: Many credit cards come with an introductory 0% APR for the first 12-18 months. This can help you manage your expenses without accruing interest, as long as you pay off the balance within the intro period.

- Manageable Repayment: After the introductory period, the interest rates are usually still lower than those of settlement loans. This makes it easier to manage your repayments.

Friends and Family

Asking friends and family for financial help can be a viable alternative. While it might be uncomfortable, it can save you from high-interest loans.

- Borrowing: Loans from friends or family usually come with little to no interest, making it a cost-effective option.

- Financial Support: This type of borrowing can provide the immediate financial relief you need without the burden of high interest rates. Just be sure to set clear terms for repayment to avoid straining relationships.

Disability Benefits

If your lawsuit involves a personal injury that prevents you from working, you might be eligible for state or federal disability benefits.

- State and Federal Assistance: Programs like Social Security Disability Insurance (SSDI) and Supplemental Security Income (SSI) can provide financial support while you wait for your settlement.

- Eligibility: Eligibility for these benefits depends on your medical condition and work history. Consult with your attorney or a disability benefits specialist to see if you qualify.

Exploring these alternatives can help you avoid the high costs and risks associated with settlement loans. In the next section, we’ll address some frequently asked questions about borrowing money until settlement.

Frequently Asked Questions about Borrowing Money Until Settlement

Can I Get a Settlement Loan Without My Attorney’s Consent?

You don’t need your attorney’s consent to apply for a settlement loan, but their involvement is crucial. Lawsuit funding companies require information about your case to evaluate its strength and potential value. This means they will need to communicate with your attorney.

While your lawyer cannot deny you the option to seek pre-settlement funding, they must provide details about your case to the funding company. This ensures that you get a fair evaluation and the financial assistance you need.

What Happens If I Lose the Case?

One of the most significant benefits of pre-settlement funding is that it is typically a non-recourse loan. This means if you lose your case, you are not required to repay the loan. The risk is on the funding company, not you.

This setup provides peace of mind, knowing that you won’t be further burdened financially if the lawsuit doesn’t end in your favor. The high interest rates on these loans help offset the risk taken by the funding company.

How Much Can I Borrow?

The amount you can borrow depends on several factors:

- Case Value: The potential value of your settlement is a primary factor. Funding companies will evaluate your case to estimate how much the settlement might be worth.

- Litigation Costs: The costs associated with your lawsuit, including attorney fees and other legal expenses, will also be considered.

- Loan Amount: Typically, you can borrow between 10% to 20% of the estimated value of your settlement. For example, if your case is expected to settle for $100,000, you might be able to borrow $10,000 to $20,000.

Each case is unique, so the exact amount you can borrow will vary. Always discuss with your attorney and the funding company to understand the specifics related to your situation.

In the next section, we’ll explore the benefits and drawbacks of settlement loans in more detail.

Conclusion

In summary, borrowing money until settlement can be a lifeline for many plaintiffs facing financial hardships. It provides immediate financial relief, allowing you to cover living expenses, medical bills, and other costs while you await the outcome of your case.

At SeaCoast Financial, we understand the challenges you face. Our goal is to offer transparent, quick, and fair pre-settlement funding to help you stay afloat during this difficult time. We work closely with your attorney to ensure a seamless process, aiming to provide you with the funds you need within 24 to 48 hours.

Making an Informed Decision

It’s crucial to weigh the benefits and drawbacks of pre-settlement funding. While it offers quick financial relief and no credit check, consider the high interest rates and the potential for long lawsuit durations. Always consult with your attorney and carefully review the terms before proceeding.

If you’re in immediate need of financial assistance while waiting for your settlement, contact us today to explore your options. We’re here to support you every step of the way, ensuring you can focus on your recovery and achieving a fair settlement.

Remember: Your financial well-being is our priority. Let us help you steer through this challenging period with ease and confidence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}